Losing a job to redundancy is stressful enough without the tax rules adding to the confusion. The reassuring part is that Australian law treats a genuine redundancy payment generously: a slice of it is completely tax-free, and much of the rest is taxed at a concessional (lower) rate rather than your normal marginal rate. This guide explains, in plain English, how the tax-free limit is worked out, the current Australian Taxation Office (ATO) figures for the 2026-27 financial year, what happens to any amount above the limit, and how your unused leave and superannuation are handled. Every dollar figure below comes from the ATO.

Key takeaways

- Only a genuine redundancy gets the tax-free limit.

- For 2026-27 the limit is $13,598 plus $6,801 for each completed year of service.

- Anything above the limit is an ETP, taxed concessionally up to the $270,000 cap.

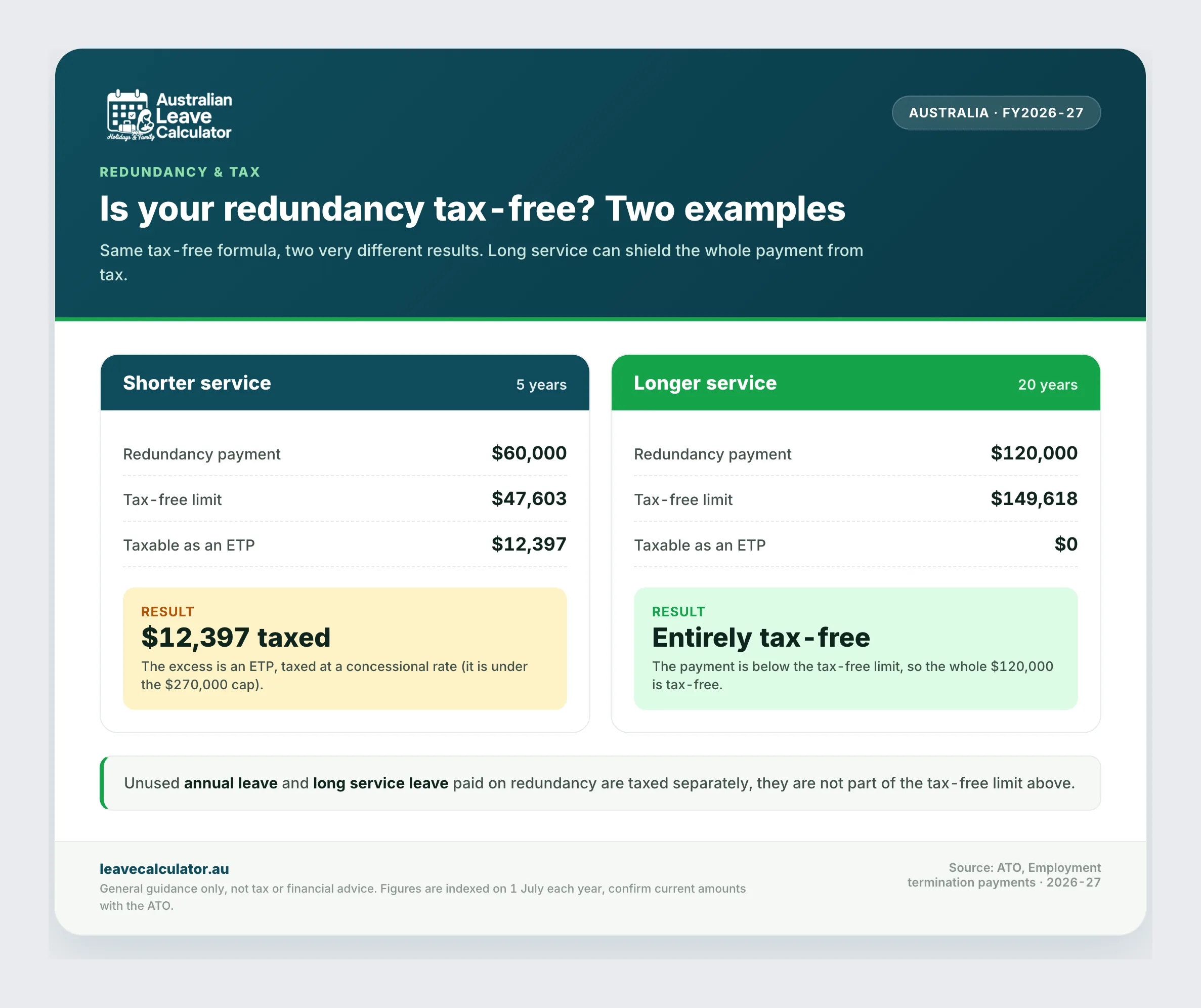

- Unused annual and long service leave payouts are taxed under separate rules.

Genuine vs non-genuine redundancy

Only a genuine redundancyqualifies for the tax-free limit. The ATO defines a genuine redundancy as one where the employer has decided the job itself no longer exists, and then dismisses the employee. The key point is that ending the employment must be the employer's decision, not the worker choosing to leave. A redundancy can still be genuine even if the employer asks for expressions of interest first, or offers a package to reduce disruption.

A payment is treated as non-genuine, and taxed as an ordinary employment termination payment (ETP) with no tax-free limit, when the worker:

- resigns or leaves voluntarily;

- is at or over their age-pension age on the day of dismissal;

- simply has a fixed-term contract run to its natural end; or

- is dismissed for disciplinary or performance reasons.

Getting this classification right matters, because it decides whether the tax-free limit applies at all. If you are not sure your situation is a true redundancy, our Fair Work Act guide, the severance pay guide and the glossary explain the underlying entitlements.

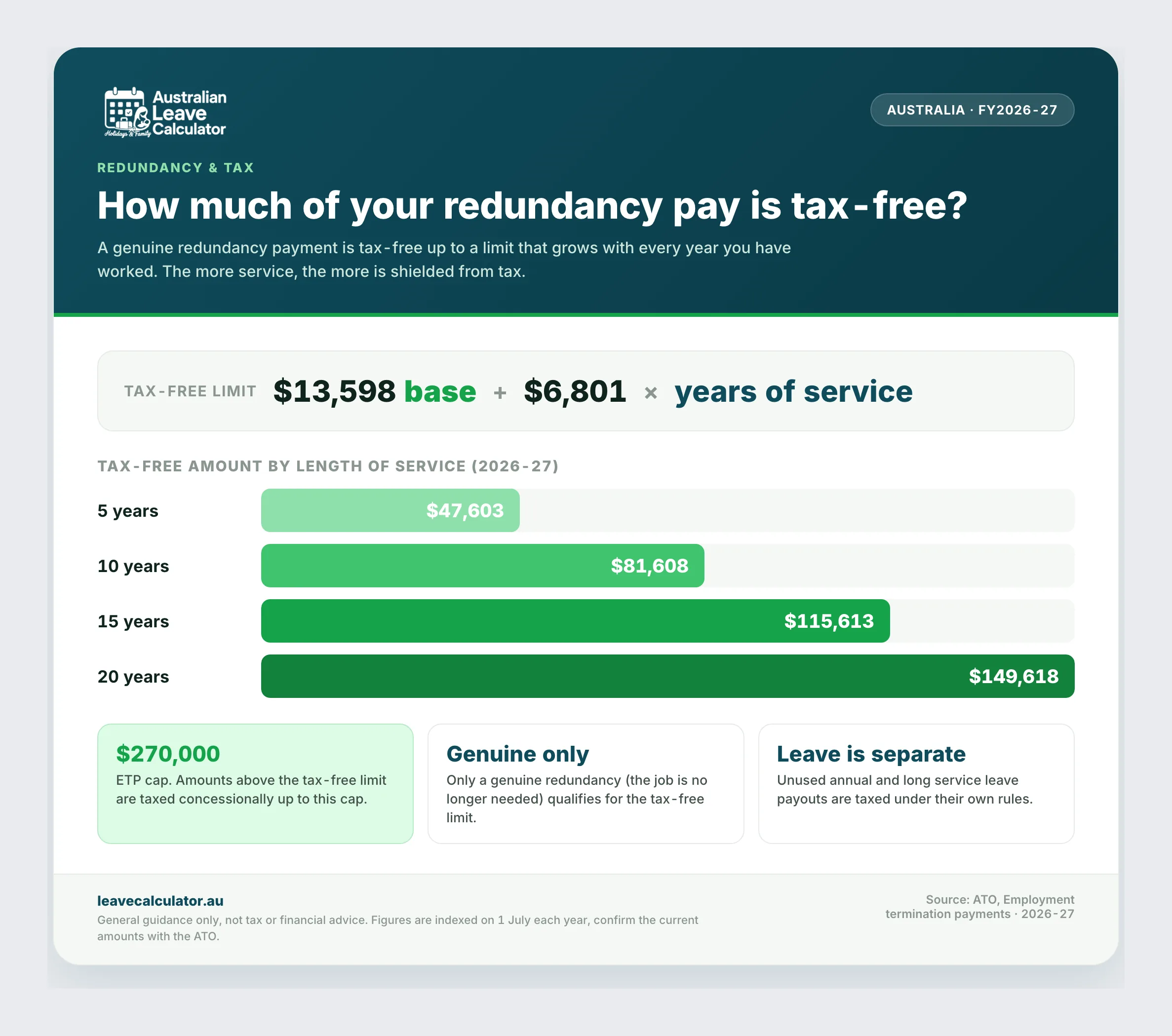

The tax-free limit formula

The tax-free part of a genuine redundancy is not a flat dollar amount. It grows with your length of service, using a simple formula:

Tax-free limit = base amount + (per-year amount × completed years of service)

Both the base amount and the per-year amount are set by the ATO and indexed on 1 July each year. The phrase completed years of service means whole years only: a part-year does not count toward the multiplier. For the 2026-27 financial year the base amount is $13,598 and the amount for each completed year of service is $6,801. So a worker with 8 completed years would have a tax-free limit of $13,598 + ($6,801 × 8) = $68,006. Anything paid up to that limit is completely free of tax and is reported at lump sum D on your income statement, not as an ETP.

Tax-free amounts by financial year

Because the figures are indexed annually, the year that matters is the one in which your employment actually ends. The table below shows the ATO base amount and per-year amount for recent financial years, so you can apply the correct pair to your own dates.

| Financial year | Base amount | For each completed year of service |

|---|---|---|

| 2026-27 | $13,598 | $6,801 |

| 2025-26 | $13,100 | $6,552 |

| 2024-25 | $12,524 | $6,264 |

| 2023-24 | $11,985 | $5,994 |

| 2022-23 | $11,591 | $5,797 |

| 2021-22 | $11,341 | $5,672 |

Above the limit: the ETP cap

Any part of a genuine redundancy that is above the tax-free limit becomes part of your ETP. It is not taxed at your full marginal rate straight away. Instead, the excess is taxed at a concessional rate up to the ETP cap, and only the amount above that cap is taxed at the top marginal rate.

The ETP cap is indexed each year in $5,000 increments. For 2026-27 the ETP cap is $270,000 (it was $260,000 in 2025-26). For most people the taxable balance of a redundancy sits comfortably below this cap, so the whole excess is taxed concessionally.

There is a second, separate limit called the whole-of-income cap. It can reduce the concessionally taxed amount by your other taxable income for the year, and it mainly affects other termination payments made at the same time, such as a gratuity or golden handshake, rather than the genuine redundancy excess itself. Where both caps could apply, the ATO uses whichever cap is lower. The tax-free part of a genuine redundancy is never touched by either cap.

Unused leave is taxed separately

A common misunderstanding is that the tax-free limit covers your unused leave as well. It does not. Any unused annual leave and unused long service leave paid out on redundancy are not part of the genuine redundancy payment and are not counted toward the tax-free limit. They are taxed under their own concessional rules.

When leave is paid because of a genuine redundancy, it is generally taxed at a flat concessional rate rather than at your marginal rate, which is usually more favourable than a normal resignation payout. The important thing for your paperwork is that these amounts are reported and taxed on their own, alongside (not inside) the redundancy figure. Our annual leave and long service leave pages explain how each entitlement accrues, and the final pay guide shows how the whole termination payslip fits together.

Superannuation treatment

Redundancy and termination payments are generally not treated as ordinary time earnings, so the compulsory super guarantee is usually not payable on a redundancy payout, on the tax-free amount, or on unused leave paid at termination. Your employer still owes super on the ordinary wages you earned up to your final day, so check that your last contribution is correct.

It is also worth knowing that an ETP cannot be rolled over into your super fund. Since 1 July 2007, employment termination payments must be paid to you directly and cannot be contributed to super, so you cannot defer the tax by pushing the money into your fund. If super treatment is central to your situation, confirm the details with your fund or a registered tax agent.

Worked examples

The two examples below use the confirmed 2026-27 ATO figures: a base amount of $13,598 plus $6,801 for each completed year of service. One shows a short-service worker where part of the payment is taxable, and one shows a long-service worker whose whole payment is tax-free.

Frequently asked questions

Is my whole redundancy payment tax-free?

Only up to the limit based on your completed years of service. In 2026-27 that is $13,598 plus $6,801 for each whole year worked. Any genuine redundancy amount above the limit becomes part of your ETP and is taxed concessionally up to the ETP cap.

Does unused annual leave or long service leave count toward the tax-free limit?

No. Unused leave is not part of the genuine redundancy payment. It is paid and taxed separately under its own concessional rules and does not use up any of the tax-free limit.

Which year's figures apply to me?

The financial year in which your employment ends. The base and per-year amounts are indexed on 1 July, so a redundancy on 30 June and one on 1 July can use different figures.

Is superannuation paid on a redundancy payment?

Generally no. A redundancy payout is usually not ordinary time earnings, so the super guarantee is not payable on it, although super is still owed on the ordinary wages you earned up to your last day.

Are the 2026-27 figures confirmed?

Yes. The ATO has published the 2026-27 genuine redundancy limits: a $13,598 base amount plus $6,801 for each completed year of service, with an ETP cap of $270,000. You can read more in our general FAQ.

Key takeaways

- Only a genuine redundancy (the job no longer exists and the employer ends the role) qualifies for the tax-free limit; a non-genuine redundancy is taxed as an ordinary ETP.

- The 2026-27 tax-free limit is $13,598 + ($6,801 × completed years of service), indexed each 1 July, and is reported at lump sum D rather than as an ETP.

- Any amount above the tax-free limit is taxed concessionally up to the $270,000 ETP cap for 2026-27, then at the top marginal rate above the cap.

- Unused annual leave and long service leave are taxed separately under their own concessional rules and are never part of the tax-free limit; super is generally not payable on the redundancy payout.

Author & reviewer

Sarah has spent over a decade advising Australian SMBs on Fair Work, NES compliance, and payroll. Based in Sydney, she has worked across hospitality, retail and professional services.