If you run or work for a small business in Australia, redundancy pay works differently from larger workplaces. Under the National Employment Standards (NES), an employer with fewer than 15 employees generally does not have to pay redundancy pay when a job is made redundant. This small business redundancy exemption trips up a lot of workers and business owners, because the way you count to 15 is not obvious, and because a small-business employee is still owed several other entitlements. This guide explains the exemption, how the headcount is done, when it is measured, what a small-business worker keeps, and when the exemption does not apply.

Key takeaways

- Businesses with fewer than 15 employees are exempt from NES redundancy pay.

- The count is a headcount and includes regular casuals and associated entities.

- Notice, accrued annual leave and long service leave are still payable.

- Employees with under 12 months service or most casuals miss out regardless of size.

The small business redundancy exemption

Most employees get their redundancy pay from the NES, which sets a scale of weeks based on years of continuous service. The NES then carves out an exception: a small business employerdoes not have to pay NES redundancy pay at all. The Fair Work Ombudsman states plainly that "most small businesses don't have to pay their employees redundancy pay under the NES."

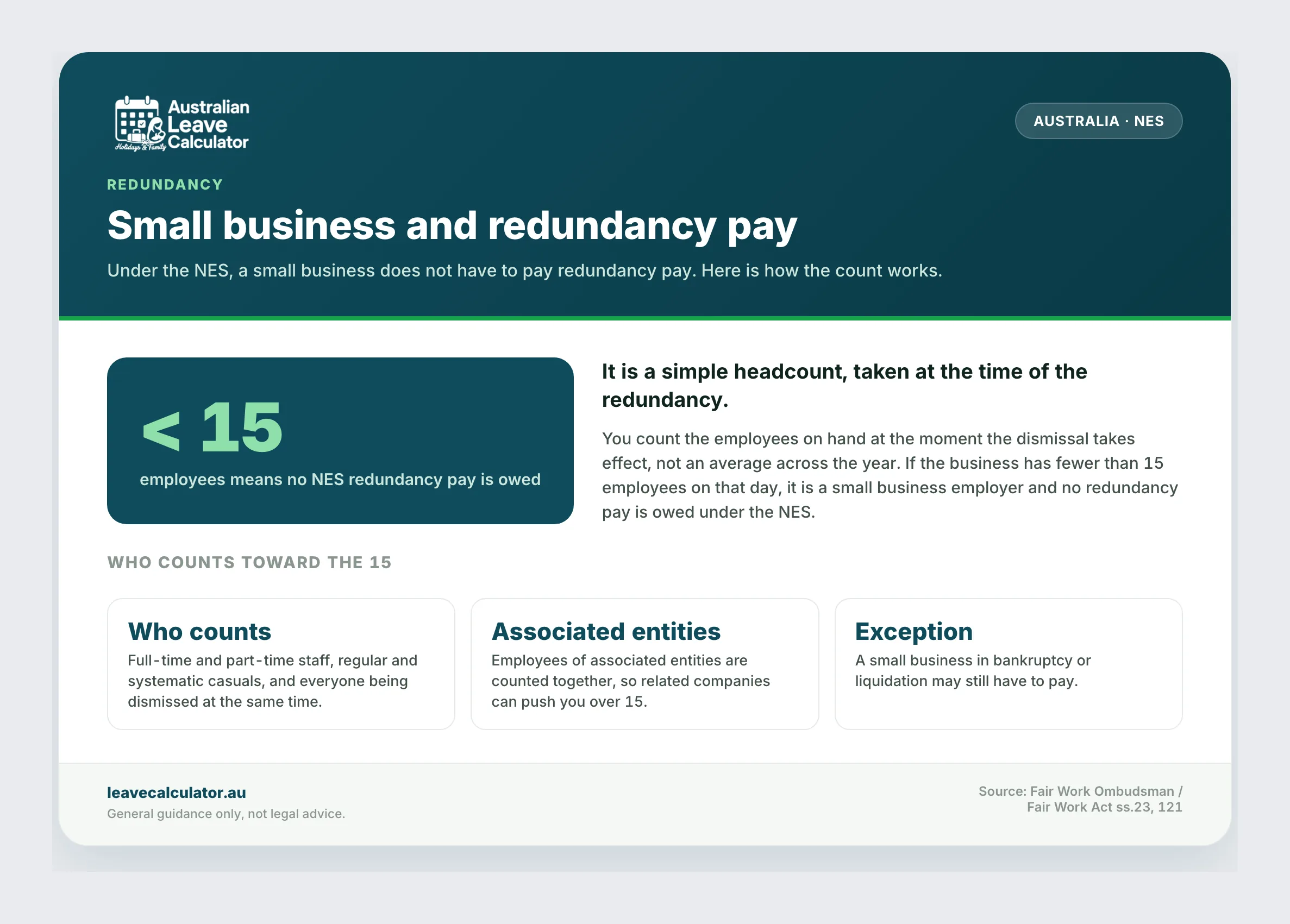

A small business employer is defined in the Fair Work Act 2009 as an employer with fewer than 15 employees. At 15 or more, the business is no longer small and NES redundancy pay applies in full. The line is exact, so the headcount matters, and getting it wrong is a common redundancy mistake in Australia.

How the 15 employees is counted

The count is a simple headcount, not a full-time-equivalent (FTE) calculation. Every person on the payroll counts as one, whether they work 38 hours a week or 8 hours a week. A business with 10 full-timers and 6 part-timers has 16 employees, so it is not a small business employer. The Act counts heads, not hours.

To work out whether an employer is a small business at the time of a redundancy, the Fair Work Ombudsman says to count all employees employed at that time, including the following.

| Worker type | Counted toward the 15? |

|---|---|

| Full-time employees | Yes |

| Part-time employees (counted as one each, not pro-rata) | Yes |

| The employee (or employees) being made redundant | Yes |

| Any other employees dismissed at the same time | Yes |

| Casuals employed on a regular and systematic basis | Yes |

| Employees of associated entities (including those based overseas) | Yes |

| Casuals who are not regular and systematic (occasional or irregular) | No |

Two of these catch people out. Regular and systematic casuals are counted, even though most casuals are excluded from redundancy pay in their own right: a casual on a predictable weekly roster is in the count, while a casual who picks up the odd shift is not. And associated entities are treated as one employer, so the staff of related companies are added together, which can quietly push a "small" business over the line.

When the headcount is taken

Timing matters because staff numbers change. The headcount is taken immediately before the termination, or at the time the employee was given notice of the termination, whichever happened first. So an employer cannot dodge redundancy pay by letting headcount drift below 15 in the weeks after notice is given; the number is fixed at the moment notice is served or employment ends. Equally, a business that has genuinely shrunk to 14 employees by the time notice is given may qualify for the exemption, subject to the downsizing rules below.

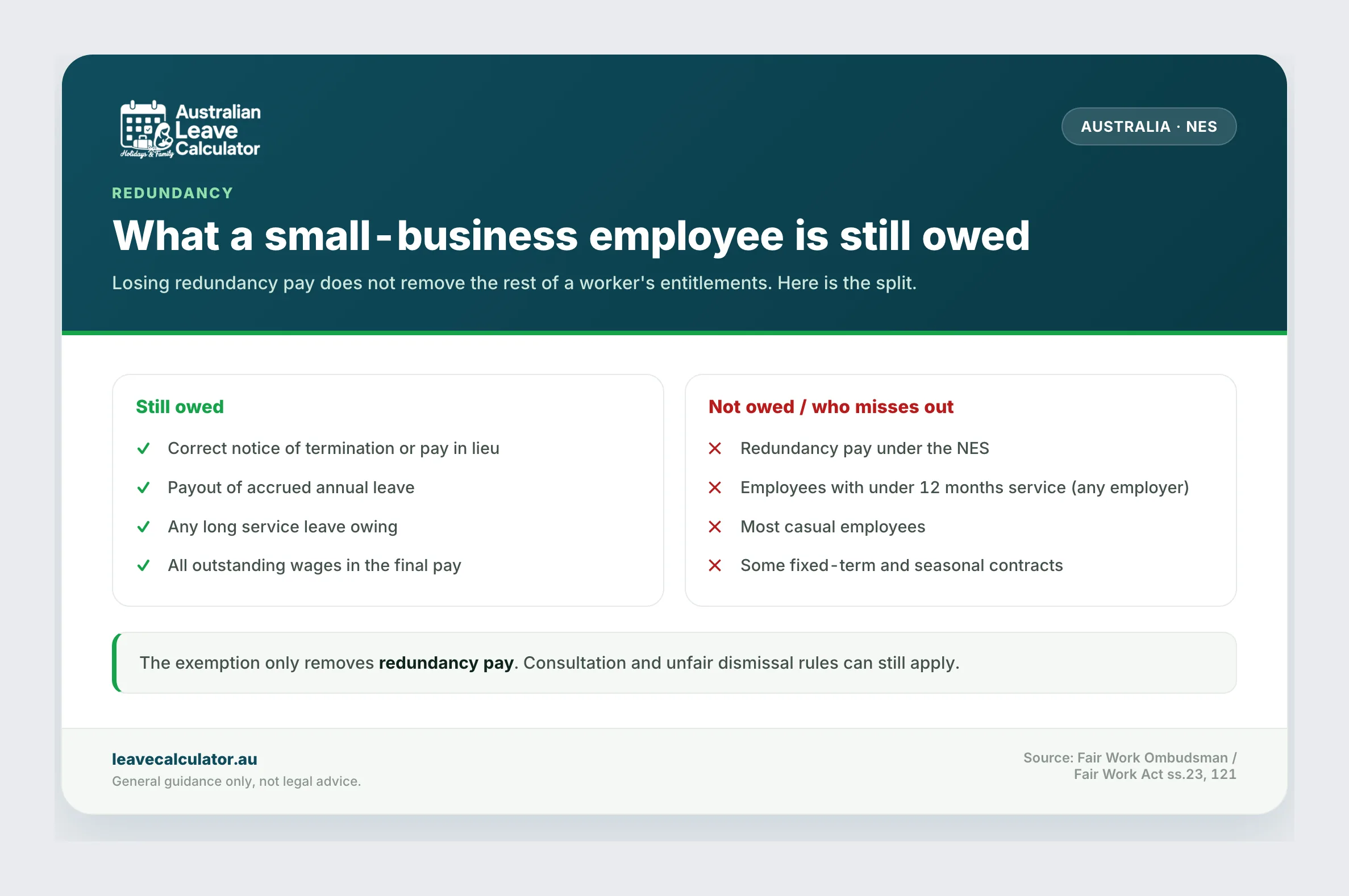

What a small-business employee is still owed

The exemption removes redundancy pay only. It does not strip away the rest of a redundant employee's entitlements. A worker made redundant by a small business is still owed the following in their final pay:

- Correct notice of termination, or payment in lieu. The NES minimum notice scale (based on age and length of service) still applies. If the employer pays it out, payment in lieu of notice must be paid on or before the day employment ends.

- Payout of accrued annual leave. Unused annual leave is paid out on termination, including annual leave loading if the employee would have received loading while employed, even where an award or contract says otherwise.

- Any long service leave entitlement. Accrued or pro-rata long service leave is paid out where the relevant state, territory or federal rules provide for it on termination.

- All outstanding wages for hours worked up to the last day, including penalty rates and allowances.

In short, "no redundancy pay" is a long way from "no final pay". Most awards require final pay within 7 days of the last day.

Other employees who miss out regardless of employer size

The 15-employee exemption is not the only reason a redundant worker may receive no redundancy pay. These employees miss out even at a large employer:

- Employees with less than 12 months of continuous service with the employer.

- Most casual employees, who are not entitled to NES redundancy pay.

- Employees engaged for a specific period, task or project, or a season (many fixed-term and seasonal workers), where the employment ends as agreed.

- Employees dismissed for serious misconduct.

- Apprentices, and trainees employed only for the length of the training arrangement.

Consultation and unfair dismissal still apply

Being exempt from redundancy pay does not exempt a small business from doing the redundancy properly. Almost all awards and enterprise agreements contain a consultation clause that requires the employer to notify affected employees, explain the changes and their effects, discuss ways to reduce the impact, and consider employees' ideas. A redundancy is only a genuine redundancy if the job is no longer needed and the employer has followed these consultation requirements.

This matters because a redundancy that is not genuine can expose even a small employer to an unfair dismissal claim. Skipping consultation, or keeping the role and simply replacing the person, can turn a lawful redundancy into an unlawful dismissal.

When a small business still has to pay

There are two situations where a business with fewer than 15 employees may still owe redundancy pay. The first is industry-specific redundancy schemes: some awards contain their own redundancy terms that apply to small businesses, so always check the relevant award or agreement rather than assuming the NES exemption applies.

The second is the downsizing exception. An employer that becomes a small business by cutting its own workforce cannot always rely on the exemption. Broadly, redundancy pay can still be owed where the employer is bankrupt or in liquidation, the employees are not covered by an industry-specific redundancy scheme, and the business became small because it terminated employees, with those terminations occurring on or after 15 December 2023. This closes a loophole where an insolvent business shed staff below 15 and then argued the remaining workers were owed nothing.

Frequently asked questions

How do I know if a casual counts toward the 15?

A casual is counted only if they are a regular and systematic casual: someone working a predictable, ongoing pattern of shifts. A casual who works occasionally or unpredictably is not counted.

Do the staff of a related company really get added in?

Yes. For the headcount, associated entities are treated as one entity, and their employees are added together, including employees based overseas. A group of small companies can add up to 15 or more employees and lose the exemption.

I work for a small business and was made redundant. Do I get anything?

Yes. You are still owed correct notice (or pay in lieu), your accrued annual leave and any long service leave, and all outstanding wages. You just may not receive NES redundancy pay. See final pay for the full list, and the glossaryor FAQ for definitions.

Is a redundancy payout taxed differently for a small business?

No. Tax treatment of any termination payment does not depend on employer size; the concessional rules for a genuine redundancy apply the same way. See redundancy tax and severance pay for how those payments are treated.

- An employer with fewer than 15 employees is a small business employer and generally does not have to pay NES redundancy pay.

- The 15 is a simple headcount: full-time and part-time staff, the employees being made redundant, regular and systematic casuals, and the staff of associated entities (including overseas) all count; irregular casuals do not.

- The count is taken immediately before termination or when notice is given, whichever is first.

- A small-business employee is still owed correct notice or pay in lieu, accrued annual leave and long service leave, and outstanding wages, and consultation and unfair dismissal rules still apply.

Author & reviewer

Sarah has spent over a decade advising Australian SMBs on Fair Work, NES compliance, and payroll. Based in Sydney, she has worked across hospitality, retail and professional services.